Insights and Analysis for Smarter Investing

Whether you're refining your investment approach or looking for fresh perspectives, our blog articles are designed to inform, inspire, and give you a competitive edge.

Accelerating the Investment Analysis Lifecycle With Collaborative AI

Accelerate the investment analysis lifecycle with human-in-the-loop AI. Learn how BPN shortens the decision-making process from weeks to just days.

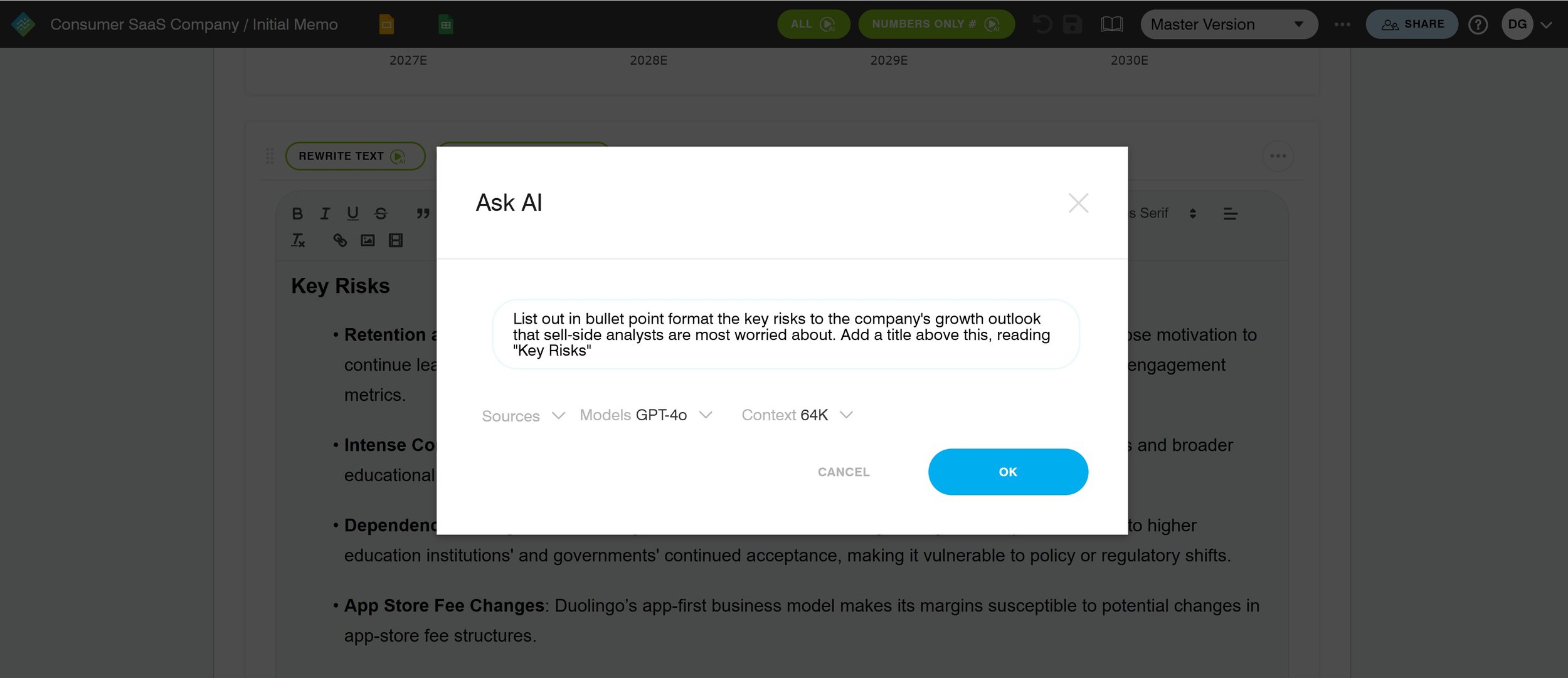

AI-Driven Investment Memos, Spreadsheet Models, and Slides Built for Modern Investment Teams

Discover how AI investment memos transform investor analysis with fast, credible, configurable automated documents to fuel efficient decision-making.

RAISE THE AI BARBELL II

Serious investors are starting to realize that AI is, in fact, transformational, but (with apologies to the one and only Maxwell Smart), too many actual users are starting to wonder “what if AI would use its powers for good, instead of evil…” OK, maybe wasting time at work isn’t exactly “evil” but it certainly won’t help you get promoted, earn more carry, or become a top decile performer. On the other hand, using AI blindly can be an evil way to embarrass yourself or make a dangerous mistake.

GOING BEYOND "SPREADSHEET/MEMO/MEETING" TO SEE THE ODDS

When evaluating my portfolio of investments, I’m often reminded of George Box’s aphorism: “All models are wrong… but some are useful”. For over 25 years, the state of the art in “useful” decision making for both company CEOs/boards and for fundamental investment committees involved a group of smart people using what I call the “Spreadsheet/Memo/Meeting process” to drive their biggest decisions.

RAISE THE AI BARBELL

If you are an investor or corporate decision-maker, I strongly doubt that AI will replace you, but you could lose your job to someone who has mastered using AI agents more effectively than you have. The speed at which AI can read and write is undeniably powerful, but off-the-shelf LLMs do a very poor job of producing the kind of insightful investment memo or compelling slide deck needed to make a mission-critical decision, and spreadsheets are notoriously challenging for LLMs.

Stay Connected

Investing moves fast, and so do we. Read more about our insights and connect with us to learn how our platform can help with your analysis process!